How should I manage my money?

Money management is the process of tracking expenses, investing, budgeting, banking, and assessing tax liabilities; it is also called investment management. Money management is a strategic technique to deliver the highest interest-output value for any amount spent on making money.

Money management is the process of tracking expenses, investing, budgeting, banking, and assessing tax liabilities; it is also called investment management. Money management is a strategic technique to deliver the highest interest-output value for any amount spent on making money.

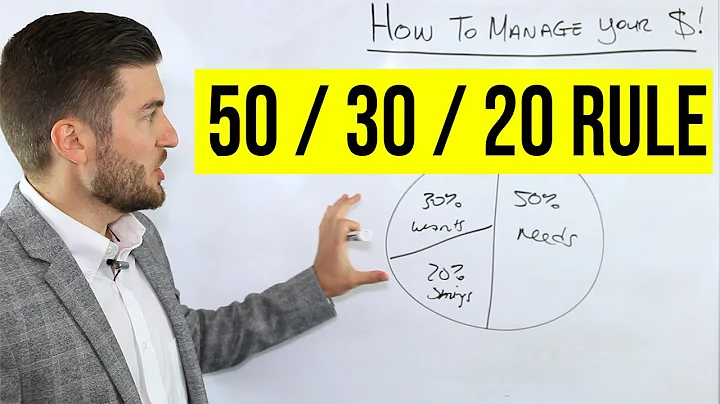

Try a simple budgeting plan. We recommend the popular 50/30/20 budget to maximize your money. In it, you spend roughly 50% of your after-tax dollars on necessities, including debt minimum payments. No more than 30% goes to wants, and at least 20% goes to savings and additional debt payments beyond minimums.

When you start managing your finances, you'll have a better perspective of where and how you're spending your money. This can help you keep within your budget, and even increase your savings. With good personal finance management, you'll also learn to control your money so you can achieve your financial goals.

Understanding how to create a realistic budget, track your spending, and set attainable savings goals are essential steps in the process. It can be overwhelming to take on all these tasks at once, but when broken down into smaller steps, money management success is achievable.

Money management refers to how you handle all of your finances, from budgeting to investing, to saving and setting goals.

One of the most common causes of financial trouble is poor budgeting. Many people spend more than they earn, and they end up using credit cards and loans to cover their expenses. This only makes their debts larger and harder to pay. In order to avoid this scenario, set a household budget.

Money management plans are used to manage cash flow—to help you identify when income is received during the month and to plan which bills and expenses to pay out of each paycheck. The weekly Money Management Plan is divided into three parts. Heavy black lines divide these parts to show priorities.

There's plenty to learn about personal financial topics, but breaking them down can help simplify things. To start expanding your financial literacy, consider these five areas: budgeting, building and improving credit, saving, borrowing and repaying debt, and investing.

1. Spend less than you make. This may seem obvious, and boring, but spending less than you make is by far the biggest key to financial success. If you struggle with spending, focus on this one rule until you're at a point where you have positive cash flow at the end of the month.

What is your biggest financial goal?

The biggest long-term financial goal for most people is saving enough money to retire. The common rule of thumb is that you should save 10% to 15% of every paycheck in a tax-advantaged retirement account like a 401(k) or 403(b), if you have access to one, or a traditional IRA or Roth IRA.

Golden Rule #1: Don't spend more than you earn

Understand the difference between needs and wants, live within your income, and don't take on any unnecessary debt. Simples.

The 50-30-20 rule recommends putting 50% of your money toward needs, 30% toward wants, and 20% toward savings. The savings category also includes money you will need to realize your future goals.

“Your income is your most important wealth-building tool. And when your money is tied up in monthly debt payments, you're working hard to make everyone else rich.”

The premise of the 30-day savings rule is straightforward: When faced with the temptation of an impulse purchase, wait 30 days before committing to the buy. During this time, take the opportunity to evaluate the necessity and impact of the purchase on your overall financial goals.

Living on $1,000 per month is a challenge. From the high costs of housing, transportation and food, plus trying to keep your bills to a minimum, it would be difficult for anyone living alone to make this work. But with some creativity, roommates and strategy, you might be able to pull it off.

Surviving on $1,000 a month requires careful budgeting, prioritizing essential expenses, and finding ways to save money. Cutting down on housing costs by sharing living spaces or finding affordable options is crucial. Utilizing public transportation or opting for a bike can help save on transportation expenses.

Feeling depressed, stressed, anxious or experiencing mania can make it difficult to manage money. For example: You might find it harder to make budgeting and spending decisions. To make yourself feel better, you might spend money you don't have on things for other people or that you don't need and then regret it later.

Also known as disordered money behaviors, it is problematic financial behaviors people adopt in an effort to cope with emotional pain. Psychology and the mental health fields have largely neglected dysfunctional money disorders.

The high cost of living, wealth inequality and job market uncertainty have all contributed to financial vulnerability, even among wealthy families.

What is your biggest financial regret?

The top regrets included not having a big enough emergency fund (mentioned by 28% of respondents), not investing aggressively enough (25%) and not buying a house when they were younger (22%).

Managed money refers to a strategy in which investors use the services of professional investment managers, who charge fees for their services. Financial advisors, wrap accounts and managed funds are three examples of professional investment managers used by investors.

Examples of leading money management firms that accept retail investors' funds include Vanguard Group Inc., Pacific Investment Management Co. (PIMCO), and J.P. Morgan Asset Management. Famous individual money managers include Warren Buffett of Berkshire Hathaway and Bruce Berkowitz of the Fairholme Fund.

We recommend the popular 50/30/20 budget to maximize your money. In it, you spend roughly 50% of your after-tax dollars on necessities, including debt minimum payments. No more than 30% goes to wants, and at least 20% goes to savings and additional debt payments beyond minimums. We like the simplicity of this plan.

Methods of saving include putting money in, for example, a deposit account, a pension account, an investment fund, or kept as cash. In terms of personal finance, saving generally specifies low-risk preservation of money, as in a deposit account, versus investment, wherein risk is a lot higher.